How I Tackled My Car Loan and Built Wealth Without Stress

Buying a car often means signing up for years of debt, but what if your car loan could fit into a smarter financial plan? I used to see my monthly payment as just another bill—until I realized it could be part of a bigger strategy. By aligning debt management with investment layout, I turned a fixed expense into a stepping stone. This is how I balanced paying off my car and growing my wealth—without overhauling my lifestyle or taking wild risks. The journey wasn’t about sudden sacrifices or risky bets. It was about making thoughtful, consistent choices that respected both my present needs and future goals. Over time, this approach reshaped how I view debt—not as an obstacle, but as a manageable element of a broader financial picture.

The Hidden Cost of Car Loans – More Than Just Monthly Payments

Many people treat a car loan as a simple transaction: borrow money, buy a car, make payments, and eventually own it. But the true cost of a car loan extends far beyond the monthly check written to the lender. Interest charges accumulate over time, often adding thousands of dollars to the original price of the vehicle. For example, a $25,000 car financed at 5% interest over five years results in nearly $3,300 in interest alone. That’s money that could have been saved, invested, or used to build an emergency fund. Yet, because the cost is spread out, it rarely feels urgent or significant in the moment.

Beyond interest, depreciation is another silent expense. A new car loses about 20% of its value the moment it’s driven off the lot and can lose up to 50% of its value within three years. This means that for much of the loan term, the borrower owes more than the car is worth—a situation known as being “upside down” on the loan. If the car is sold or totaled in an accident during this period, the owner may still owe the lender thousands, even after losing the asset. This risk is often overlooked when the focus is solely on affordability of the monthly payment.

Equally important is the concept of opportunity cost—the value of what you give up by choosing one financial path over another. Every dollar spent on a car loan is a dollar not available for investment. If that same dollar were invested in a diversified portfolio earning an average annual return of 7%, it could double in about ten years. Over the life of a five-year car loan, the cumulative opportunity cost can be substantial. Many individuals fail to consider this trade-off, treating the car payment as an unavoidable expense without questioning whether a more strategic approach might exist. Recognizing these hidden costs is the first step toward transforming a routine debt into a component of a smarter financial plan.

Why Debt and Investing Aren’t Enemies – A Mindset Shift

Conventional financial wisdom often promotes the idea that all debt must be eliminated before investing. While this approach offers emotional comfort and reduces financial complexity, it isn’t always the most effective strategy—especially when dealing with low-interest debt. The key lies in distinguishing between harmful debt, such as high-interest credit cards, and manageable debt, like a car loan with a favorable interest rate. When the cost of borrowing is relatively low, and potential investment returns are higher, it can make sense to maintain the debt while directing additional funds toward growth-oriented assets.

Consider this: if a car loan carries an interest rate of 4%, and the historical average return of the stock market is around 7% annually, investing surplus cash may yield a net positive outcome over time. This doesn’t mean ignoring debt repayment, but rather prioritizing it strategically. Instead of funneling every extra dollar into early payoff, a balanced approach allocates resources to both debt reduction and investment growth. The goal is not to avoid responsibility, but to optimize financial efficiency.

This mindset shift requires a move away from viewing debt solely as a burden. Instead, it’s reframed as a tool—one that, when used wisely, can coexist with wealth-building efforts. For many, especially those in their 30s and 40s managing multiple financial responsibilities, this balance is essential. It allows for progress on multiple fronts: maintaining a reliable vehicle for family needs while simultaneously building long-term security. The emotional relief of being debt-free is valuable, but so is the peace of mind that comes from knowing your money is working for you in more than one way.

Of course, this strategy depends on discipline and consistency. It requires a clear understanding of interest rates, investment time horizons, and personal risk tolerance. It also assumes that minimum payments are reliably made and that no additional high-interest debt is accumulated. When these conditions are met, the coexistence of debt and investing becomes not only possible but advantageous. The real enemy isn’t debt itself, but a rigid financial mindset that prevents optimization.

Matching Loan Terms with Investment Horizons – Timing Is Key

Financial success often hinges on timing—specifically, how well your debt obligations align with your investment goals. A car loan typically lasts three to seven years, placing it in the short-to-medium-term category. To maximize financial efficiency, it’s wise to pair this timeline with investment vehicles that offer growth potential without locking up funds for decades. This synchronization prevents cash flow conflicts and ensures that money is available when needed, whether for unexpected repairs, family emergencies, or planned life events.

For instance, investing in a retirement account like a 401(k) or IRA offers long-term benefits, but early withdrawals usually come with penalties and tax consequences. If too much money is tied up in long-term investments while managing a car loan, liquidity may become strained. A better approach is to balance long-term accounts with more accessible options, such as taxable brokerage accounts or high-yield savings accounts. These allow flexibility to adjust allocations as financial priorities shift, without disrupting debt repayment progress.

Another timing consideration is the interest rate environment. When inflation is moderate and investment returns are steady, the gap between loan costs and potential gains is more favorable. During such periods, maintaining a low-interest car loan while investing surplus funds can be a prudent choice. However, if interest rates rise significantly or market volatility increases, the risk profile changes. In those cases, accelerating debt repayment may become the more conservative and appropriate strategy.

The goal is not to predict market movements perfectly, but to build a structure that adapts to changing conditions. By aligning the duration of the car loan with investment timelines, individuals can avoid the stress of mismatched financial commitments. This approach supports both short-term stability and long-term growth, creating a rhythm in personal finance that feels sustainable rather than reactive. When timing is respected, debt doesn’t compete with investing—it complements it.

Building a Dual-Track Plan: Pay Down Debt While Growing Assets

The most effective financial strategies are not built on extremes, but on balance. A dual-track plan allows individuals to make consistent progress on two fronts: reducing debt and growing wealth. This method avoids the all-or-nothing mindset that often leads to burnout or financial strain. Instead, it promotes steady, manageable actions that compound over time. The foundation of this plan is discipline—setting clear priorities and sticking to them, even when progress feels slow.

The first track focuses on the car loan. This means making on-time payments every month, ideally through automatic transfers that remove the temptation to delay or skip. If possible, adding even a small extra amount—$25 or $50 per month—can reduce the total interest paid and shorten the loan term. The key is consistency, not size. Over five years, an extra $30 per month on a $25,000 loan at 5% interest can save over $400 in interest and shave several months off the repayment period.

The second track is dedicated to investing. Even modest contributions, such as $100 per month, can grow significantly over time thanks to compound returns. Setting up automatic transfers to an investment account ensures that saving becomes a habit, not a choice. This track doesn’t require large sums or complex decisions. It simply requires regularity. Over a decade, $100 per month invested at a 7% annual return grows to more than $17,000—enough to cover a future car purchase or supplement retirement savings.

What makes this dual-track approach powerful is its sustainability. It doesn’t demand drastic lifestyle changes or perfect financial conditions. It works within real-world constraints—busy schedules, fluctuating incomes, and competing priorities. By treating both debt repayment and investing as non-negotiable habits, individuals create a rhythm that supports long-term financial health. The progress may seem small at first, but over time, the combined effect of reduced debt and growing assets builds real momentum.

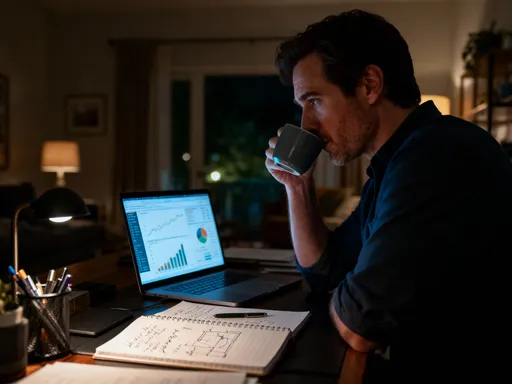

Choosing the Right Investment Layout – Safety, Growth, and Access

Not every investment is suitable for someone managing a car loan. The right choices depend on individual goals, risk tolerance, and the need for liquidity. The objective isn’t to chase high returns at all costs, but to build a portfolio that supports stability while allowing for growth. This means prioritizing diversification, low fees, and accessibility—principles that protect capital while positioning it to grow over time.

For many, a diversified exchange-traded fund (ETF) or index fund offers an ideal starting point. These funds spread risk across hundreds or thousands of companies, reducing the impact of any single market fluctuation. They also tend to have lower expense ratios than actively managed funds, which means more of the returns stay with the investor. A broad-market ETF, such as one tracking the S&P 500, has historically delivered average annual returns of about 7% to 10% over long periods, making it a reliable option for long-term growth.

At the same time, not all investments need to be in the stock market. High-yield savings accounts and money market funds play an important role, especially for funds that may be needed in the near future. These accounts offer modest returns—typically between 3% and 5% annually—but with virtually no risk of loss. They serve as a bridge between emergency savings and long-term investments, providing a safe place to park money while still earning interest.

Retirement accounts like IRAs and 401(k)s also fit into this layout, particularly when employer matching is available. Contributing enough to get the full match is often described as “free money,” and for good reason—it’s an immediate return on investment. Even after accounting for tax implications and withdrawal rules, these accounts offer powerful long-term advantages. The key is to integrate them into the overall plan without overcommitting at the expense of short-term stability.

Ultimately, the right investment layout is one that feels manageable and aligned with personal circumstances. It doesn’t require picking individual stocks or timing the market. It’s about making consistent, informed choices that support both debt management and wealth accumulation. When safety, growth, and access are balanced, the result is a financial foundation that can withstand life’s uncertainties.

Risk Control: Avoiding Overextension and Emotional Traps

Even the most well-designed financial plan can fail without proper safeguards. Risk control is not about avoiding all danger—it’s about managing exposure and building resilience. One of the most common pitfalls is overextending, whether by taking on too large a car loan, investing too aggressively, or cutting essential expenses to accelerate debt payoff. Each of these actions may seem justified in the moment, but they can lead to financial strain and emotional burnout over time.

An emergency fund is one of the most effective risk controls. Having three to six months’ worth of living expenses set aside in a liquid account provides a buffer against unexpected events, such as job loss, medical bills, or car repairs. Without this cushion, even a minor setback can force someone to rely on credit cards or loans, undoing months of progress. The emergency fund should be separate from both debt repayment and investment accounts, treated as a safety net rather than a source of growth.

Realistic budgeting is another essential component. It’s easy to create an idealized plan that assumes perfect discipline, but real life includes surprises and fluctuations. A sustainable budget accounts for occasional treats, fluctuating utility bills, and irregular expenses like school supplies or holiday gifts. By building flexibility into the plan, individuals are less likely to abandon it when reality doesn’t match expectations.

Emotional discipline is equally important. Financial decisions are often influenced by fear, excitement, or social pressure. The desire to be completely debt-free can lead to overpaying on low-interest loans at the expense of long-term investing. Conversely, the allure of high returns can tempt people into risky investments they don’t fully understand. Staying focused on the long-term strategy—rather than reacting to short-term emotions—requires self-awareness and patience.

Regular check-ins, such as quarterly financial reviews, help maintain perspective. These moments allow for adjustments based on changes in income, expenses, or goals, without derailing the overall plan. By incorporating risk controls from the start, individuals create a financial structure that is not only effective but durable.

From Car Loan to Financial Freedom – A Sustainable Path Forward

The journey of managing a car loan doesn’t have to end with the final payment. When approached strategically, it can become a stepping stone toward broader financial freedom. The lessons learned—about timing, balance, discipline, and risk management—apply far beyond a single debt. They form the foundation of a lifelong approach to money that values both responsibility and growth.

Financial freedom isn’t defined by the absence of debt, but by the presence of choice. It means having enough savings to handle emergencies, enough investments to grow wealth, and enough confidence to make decisions based on values rather than fear. By treating the car loan as part of a larger plan, rather than an isolated burden, individuals gain control over their financial narrative.

The power of small, consistent actions cannot be overstated. Paying a little extra on the loan, investing a modest amount each month, building an emergency fund—none of these steps require dramatic changes. But over time, their combined effect creates meaningful progress. Compound growth works not just in investments, but in habits. The more often a person makes a thoughtful financial decision, the more natural it becomes.

For women in their 30s to 50s, who often juggle family, career, and caregiving responsibilities, this balanced approach offers both practicality and peace of mind. It acknowledges real constraints while providing a path forward. It doesn’t promise overnight riches or eliminate all risk, but it builds resilience and momentum. And in the end, that’s what true financial well-being looks like—not perfection, but steady, sustainable progress toward a life of greater freedom and security.