How I Mastered Asset Allocation While Juggling Installment Payments

What if paying in installments could actually help you build wealth instead of draining it? I used to see monthly payments as just another financial burden—until I flipped the script. By aligning my installment commitments with smarter asset allocation, I turned cash flow stress into long-term growth. This isn’t about cutting costs or earning more; it’s about working with what you already have. Here’s how I restructured my finances to make every dollar pull double duty. The journey began not with a windfall or a career leap, but with a simple realization: my recurring payments weren’t just expenses—they were part of a larger financial rhythm that, if managed correctly, could support investment rather than hinder it. This shift in perspective changed everything.

The Hidden Cost of Installment Payments (And Why Most People Miss It)

Installment payments are everywhere—on electronics, furniture, gym memberships, even groceries. They offer immediate access to goods and services without the need for large upfront costs. At first glance, this seems like financial convenience. But beneath the surface lies a hidden cost that most people overlook: the erosion of financial flexibility. When multiple installment obligations fill up your monthly budget, they leave little room for strategic investing or emergency preparedness. The real price isn’t just the interest charged—it’s the opportunity cost of not being able to deploy capital elsewhere. Many consumers focus solely on whether a payment fits within their current income, without considering how that commitment affects their long-term financial trajectory.

I learned this lesson the hard way. A few years ago, I upgraded my home office setup, signed up for a premium streaming bundle, and financed a new appliance—all on installment plans. Individually, each payment seemed manageable. But collectively, they consumed nearly 30% of my after-tax income. At the time, I didn’t think much of it. I was making ends meet, and my credit score remained strong. What I failed to see was how these recurring outflows were quietly pushing investment goals further into the future. Every dollar going toward interest or minimum payments was a dollar not compounding in a diversified portfolio. It wasn’t until I mapped out all my obligations on a 12-month cash flow calendar that the full picture emerged: I had prioritized short-term comfort over long-term security.

This misalignment between spending and saving is more common than many realize. Behavioral finance studies show that people tend to underestimate the cumulative impact of small, regular payments. Because each transaction feels low-stakes, they don’t trigger the same level of scrutiny as a major purchase. Yet over time, these obligations act like financial anchors, limiting mobility and reducing the ability to respond to market opportunities. For instance, when a promising investment window opened—a dip in index fund prices during a market correction—I couldn’t act because my cash flow was already committed. That moment was a wake-up call. I realized that installment plans, while useful, must be integrated into a broader financial strategy rather than treated as isolated transactions. Otherwise, they become silent obstacles to wealth building.

Asset Allocation Isn’t Just for the Wealthy—It’s for Everyone With a Payment Plan

Many people believe asset allocation is a strategy reserved for high-net-worth individuals with surplus capital. They assume you need thousands in disposable income before considering how to divide investments among stocks, bonds, and cash. But this mindset misses a crucial truth: asset allocation begins the moment you have income and obligations. Even if you're making installment payments, you're already managing a financial portfolio that includes both liabilities and potential growth assets. The key is to treat your entire cash flow—both inflows and outflows—as part of a dynamic system that can be optimized for long-term outcomes.

When I shifted my perspective, I stopped seeing my monthly payments as mere expenses. Instead, I began viewing them as scheduled outflows that needed to be balanced with intentional inflows—such as automated contributions to investment accounts. This change in framing allowed me to think holistically about my financial picture. For example, I realized that financing a laptop over 12 months wasn’t just a debt obligation; it was also an investment in productivity that could generate future income. By recognizing this, I justified allocating a portion of my earnings toward both the payment and a parallel investment in a low-cost index fund. The two weren’t mutually exclusive—they could coexist within a well-structured plan.

Asset allocation, in this context, means more than picking stocks. It involves aligning your purchasing decisions, debt schedule, and investment rhythm so that they support one another. For instance, if you know a large installment payment is due in six months, you might temporarily reduce exposure to volatile assets and increase holdings in stable, income-generating instruments like dividend-paying stocks or short-term bonds. This way, you protect your liquidity while still allowing your portfolio to grow. The goal isn’t to eliminate installment plans but to ensure they don’t disrupt your financial equilibrium. Anyone can adopt this approach, regardless of income level. What matters is consistency, awareness, and a commitment to treating every dollar as a tool for building long-term value.

Syncing Cash Flow With Investment Cycles: A Practical Framework

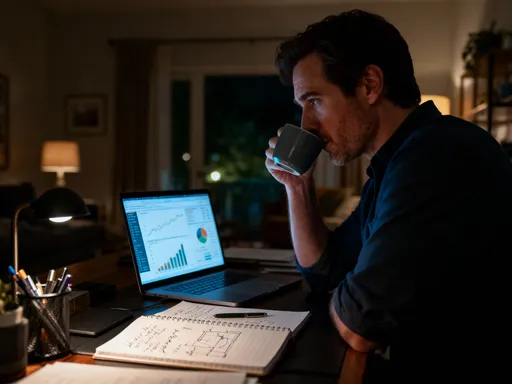

One of the most transformative steps I took was aligning my investment contributions with my installment due dates. This might sound minor, but the impact was significant. Before, I would make investments whenever I had leftover funds at the end of the month—often after all the bills were paid. But by then, my account balance was low, and I frequently missed contribution windows or invested irregularly. This reactive approach led to inconsistent growth and missed compounding opportunities. Once I started planning investments in tandem with my payment calendar, everything changed.

My new system works like this: I identify the days when major installment payments clear my account—usually around the 10th and 25th of each month. Instead of scheduling investments on those dates, I set up automatic transfers for the 5th and 20th, ensuring funds are allocated before the larger outflows occur. This creates a buffer and prevents cash shortages. Additionally, I time dividend reinvestments and mutual fund purchases for the end of the month, when my cash flow stabilizes and any remaining income can be deployed efficiently. This rhythmic approach turned my financial management from chaotic to predictable, reducing stress and increasing discipline.

Another critical element of this framework is adjusting asset types based on cash flow pressure. During months with heavier installment loads, I shift a portion of my portfolio toward low-volatility holdings such as bond funds or money market accounts. These assets provide stability and preserve capital when liquidity is tight. Conversely, in months where installment obligations are lighter—such as after paying off a short-term loan—I increase exposure to growth-oriented assets like equity index funds. This cyclical rebalancing allows me to take advantage of market opportunities without overextending myself. Over time, this method has improved my risk-adjusted returns and reduced emotional decision-making. It’s not about market timing; it’s about personal cash flow timing, which is far more within your control.

Risk Control: How Installments Can Expose You (And How to Protect Yourself)

Every installment plan introduces financial exposure. While it may feel like a simple payment agreement, it’s essentially a form of leverage—a commitment to pay future income for present consumption. When multiple installment obligations overlap, they can create a hidden debt burden that amplifies financial risk, especially during periods of income disruption. I underestimated this risk until I experienced a temporary reduction in freelance work. My regular income dipped for three months, and suddenly, my installment payments—which had seemed manageable—became a serious strain. My emergency fund covered basic living expenses, but it wasn’t enough to maintain both payments and investment contributions.

Faced with a cash shortfall, I made the difficult decision to sell a portion of my investment portfolio to cover obligations. Unfortunately, I did so during a market downturn, locking in losses on assets that later recovered. That experience was a painful but valuable lesson: installment commitments must be balanced with liquidity and downside protection. I realized that simply having an emergency fund wasn’t sufficient. I needed a structural safeguard within my investment strategy itself—a buffer that could absorb temporary shocks without forcing me to sell at inopportune times.

To address this, I now allocate a portion of my portfolio to accessible, stable assets that serve as a financial cushion. Specifically, I maintain a tiered approach: 20% of my investable assets are held in high-yield savings accounts and short-term Treasury instruments. These are not meant for long-term growth but for liquidity and stability. Another 30% is in dividend-paying stocks and bond funds that generate regular income, which I can tap if needed without selling principal. The remaining 50% is invested in growth assets with a long-term horizon. This structure ensures that even if my income fluctuates, I have options that don’t require panic-driven decisions. By integrating risk control into my asset allocation model, I’ve made my financial system more resilient—not just against market volatility, but against life’s inevitable uncertainties.

The 3-Step Rebalancing Trick That Keeps Me on Track

Financial plans don’t stay relevant on their own. Life changes—salaries shift, family needs evolve, economic conditions fluctuate. My original strategy worked well for a while, but it began to fray when unexpected expenses arose and investment returns varied. I needed a way to keep my system dynamic without becoming overwhelming. That’s when I developed a simple quarterly rebalancing routine: a three-step process that takes less than an hour but keeps my finances aligned with my goals.

The first step is reviewing all upcoming installment obligations. I pull up my payment calendar and list every scheduled payment for the next 90 days—everything from subscription renewals to loan installments. This gives me a clear picture of my near-term cash flow demands. The second step is assessing my current asset allocation. I check how my investments are distributed across asset classes and compare them to my target ratios. If one category has grown disproportionately—say, equities have surged due to a bull market—I note the imbalance. The third step is adjustment: I either redirect new contributions to underweighted areas or make small reallocations to restore balance. This might mean pausing a particular investment for a month to free up cash or shifting a percentage from stocks to bonds to maintain risk levels.

This routine has proven remarkably effective. It prevents complacency and ensures that my strategy evolves with my circumstances. One quarter, I received a year-end bonus that allowed me to pay off a high-interest installment plan early. Instead of spending the surplus, I used the rebalancing process to redirect future payments into a diversified ETF. Another quarter, a medical expense required temporary reallocation from growth assets to cash holdings. Because I reviewed my plan regularly, the adjustment was smooth and intentional, not reactive. The beauty of this system is its simplicity. It doesn’t require complex tools or daily monitoring—just disciplined, periodic review. For anyone managing installment payments alongside investment goals, this three-step check can be a game-changer.

From Consumer to Investor: Changing the Mindset That Changed My Results

The most powerful change I made wasn’t technical—it was psychological. For years, I saw myself primarily as a consumer: someone who made purchases and paid bills. My financial identity revolved around spending decisions. But when I began treating my installment payments as part of a broader financial strategy, my self-perception shifted. I started seeing myself as an investor managing cash flow, not just a buyer deferring payment. This mental transformation had a profound impact on my behavior. Every purchase decision became a financial trade-off: Is this payment worth delaying my next investment milestone? Could I use this financing opportunity to preserve capital for higher-return investments?

This new mindset led to more intentional buying habits. I no longer signed up for installment plans out of convenience alone. I evaluated each one based on its impact on my overall financial posture. Some purchases I deferred; others I accepted strategically because they freed up cash for more important goals. For example, financing a reliable used car allowed me to avoid draining my savings, so I could maintain consistent contributions to my retirement account. The payment wasn’t just an expense—it was a tactical move within a larger wealth-building strategy. Over time, this approach reduced impulsive spending and increased financial confidence.

Moreover, I began to view credit not as a trap but as a tool—when used responsibly. I focused on installment plans with low or zero interest, ensuring that the cost of financing didn’t outweigh the benefits. I also prioritized plans that aligned with my income cycle, such as starting new payments at the beginning of a quarter when my cash flow was strongest. This level of intentionality transformed my relationship with money. I wasn’t just surviving month to month; I was designing a sustainable financial path. The shift from consumer to allocator didn’t happen overnight, but once it took root, it became the foundation of lasting progress.

Building a Sustainable System: Long-Term Gains Over Short-Term Fixes

Quick fixes rarely lead to lasting financial health. Budgeting apps, expense trackers, and temporary spending cuts can provide short-term relief, but they don’t address the underlying structure of your finances. What I’ve built is not a diet but a lifestyle—a sustainable system that integrates installment payments into a coherent asset allocation strategy. The goal isn’t perfection; it’s consistency, awareness, and continuous improvement. I no longer fear payments. I plan for them, work around them, and sometimes even use them to my advantage.

The core principles that keep this system working are alignment, protection, and discipline. First, I align my outflows and inflows so that investment activity complements rather than competes with payment obligations. Second, I build in proactive risk management through diversified, liquid holdings that act as a buffer during downturns. Third, I maintain disciplined rebalancing through regular review, ensuring that my strategy adapts to changing circumstances without losing sight of long-term goals. These principles are not dependent on high income or market timing. They rely on structure, not willpower.

Today, my installment payments no longer feel like burdens. They are part of a rhythm that supports growth. I’ve seen my net worth increase steadily, not because I earned more or cut every expense, but because I made better use of the resources I already had. This approach is accessible to anyone willing to rethink the relationship between spending and investing. It’s not about eliminating installment plans—it’s about transforming them from wealth drains into components of a smarter financial system. By mastering asset allocation while juggling payments, I’ve turned what once felt like a limitation into a source of strength. And if I can do it, so can you.